The Singapore Overnight Rate Average (SORA) has emerged as a crucial benchmark in Singapore’s financial landscape, particularly following the transition from SIBOR and SOR to SORA. This shift reflects global trends towards risk-free rate benchmarks, ensuring greater transparency and stability in financial markets. Among the key metrics derived from SORA are the compounded 1-month and 3-month rates, which play pivotal roles in pricing loans and other financial products. Therefore it is important to have a better understanding of SORA especially more so for homeowners in Singapore who have taken up a home loan with a major financial institution/bank.

What is SORA?

SORA is the volume-weighted average rate of unsecured overnight interbank lending transactions in Singapore. It is administered by the Monetary Authority of Singapore (MAS) and represents a near risk-free rate. Unlike its predecessors, SORA is backward-looking, and based on actual transactions, making it a reliable reflection of market conditions.

Compounded 1-Month and 3-Month SORA

The compounded 1-month and 3-month SORA rates are derived by compounding the daily SORA rates over the respective time periods. These rates smooth out daily volatility and provide a stable reference for financial instruments. The 1-month rate is commonly used for short-term loans and financial agreements, while the 3-month rate serves as a benchmark for medium-term lending and investment products.

SORA Replacing SIBOR and SOR for Home Loans

The replacement of SIBOR and SOR with SORA for home loans marks a significant change in Singapore’s financial framework. SORA’s adoption provides borrowers with a more transparent and market-driven interest rate benchmark, aligning with global best practices. Compared to SIBOR and SOR, SORA offers greater stability as it is derived from actual overnight interbank lending rates. This transition aims to enhance the resilience and efficiency of Singapore’s financial system while offering homebuyers a more predictable loan reference rate.

Importance and Applications

The adoption of compounded SORA rates has significant implications for borrowers and lenders. They are widely used in floating-rate loan agreements, providing a more stable and predictable interest rate compared to daily fluctuations. For instance, home loans pegged to the 3-month compounded SORA offer borrowers the advantage of transparency and reduced interest rate volatility.

Additionally, financial institutions utilize these rates for hedging and risk management, given their alignment with market realities. The transition to SORA benchmarks underscores a broader move towards robust financial systems anchored on transparency and reliability.

Current Trends

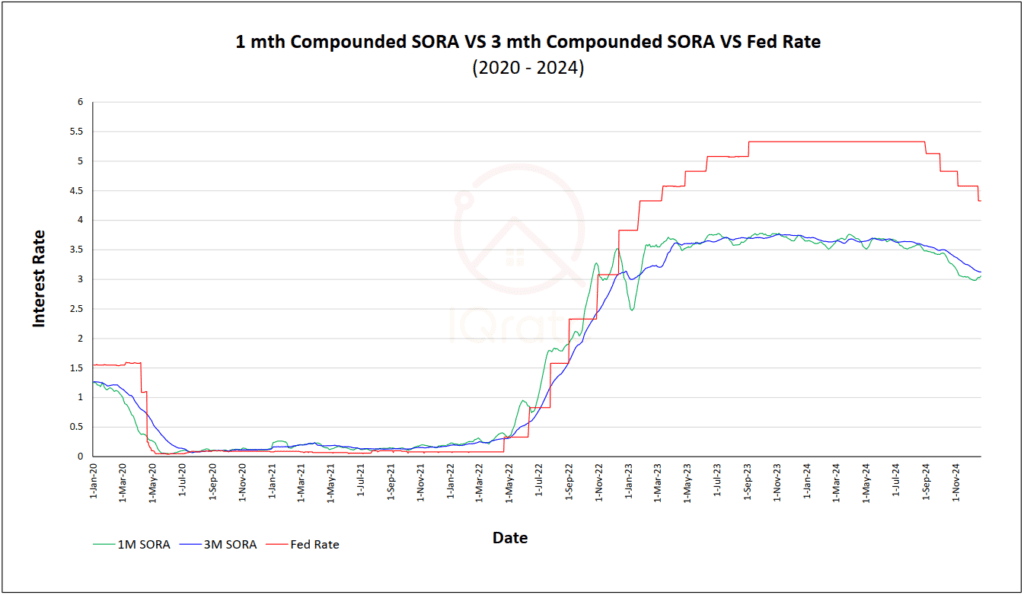

Recent trends in compounded 1-month and 3-month SORA rates reflect economic conditions and monetary policies. During periods of tightening monetary policies, these rates tend to rise, impacting loan affordability. Conversely, during economic easing, borrowers benefit from lower rates.

SORA Interest Rates & Trend for 2020 – 2024

Conclusion

As Singapore continues to embrace SORA as its primary interest rate benchmark, understanding compounded 1-month and 3-month rates becomes essential for stakeholders. These metrics not only ensure consistency with international standards but also foster a resilient and transparent financial ecosystem.

Your financial future starts with the right advice

In the ever-evolving landscape of home loans in Singapore, making informed decisions is key to securing your financial future.

Our dedicated team of expert mortgage brokers from IQrate is here to guide you every step of the way. Don’t let uncertainty hold you back; take the first step towards maximizing savings for your mortgage loan, often your largest financial commitment.

Contact us now to schedule a personalised and free consultation.