One of the biggest surprises for many property buyers in Singapore is discovering that the amount they can borrow isn’t determined solely by their income.

You may earn a healthy salary, have substantial CPF savings, and excellent credit history, but still receive a loan offer that falls short of your expectations.

Why?

The answer often lies in the Total Debt Servicing Ratio (TDSR).

Whether you’re buying your first home, upgrading from an HDB flat to a condominium, purchasing an Executive Condominium (EC), or refinancing an existing mortgage, understanding TDSR is essential.

In this guide, IQrate explains everything you need to know about TDSR, including how banks calculate it, what income counts, what debts are included, and practical strategies to improve your borrowing capacity.

Quick Summary

If you only remember five things about Total Debt Servicing Ratio (TDSR), remember these:

- TDSR limits your total monthly debt obligations to 55% of your gross monthly income.

- Banks assess more than just your salary; they also consider existing loans, age, loan tenure, and other commitments.

- Not all income is treated equally. Bonuses, commissions, rental income, and self-employed income may be assessed differently.

- Passing TDSR does not automatically guarantee loan approval.

- Speaking to an independent mortgage adviser before committing to a purchase can help you understand your financing options.

Myth vs Fact

| Myth | Fact |

| TDSR is based only on salary. | Banks assess both income and existing debt obligations. |

| CPF increases my TDSR. | CPF savings are not treated as income. |

| All banks calculate income the same way. | Assessment policies can differ between lenders. |

| Passing TDSR guarantees approval. | The lender still performs its overall credit assessment. |

What Exactly Is TDSR?

The Total Debt Servicing Ratio (TDSR) is a framework introduced by the Monetary Authority of Singapore to promote prudent borrowing.

It limits the proportion of a borrower’s gross monthly income that can be used to service debt obligations.

Currently, the maximum TDSR is: 55% of Gross Monthly Income

This means that the total monthly repayments for all eligible debt obligations, including your proposed home loan, should generally not exceed 55% of your gross monthly income.

Why Was TDSR Introduced?

Before the Total Debt Servicing Ratio (TDSR) framework was implemented in 2013, some borrowers took on debt levels that left little room to cope with interest rate increases or income disruptions.

The framework was introduced to:

- Encourage responsible borrowing/lending

- Reduce household over-leverage

- Strengthen financial resilience

- Support long-term stability in Singapore’s property market

Instead of focusing only on the home loan, TDSR considers your overall debt obligations.

Which Properties Are Subject to TDSR?

Total Debt Servicing Ratio (TDSR) generally applies when obtaining loans for:

- Private condominiums

- Landed properties

- Executive Condominiums (bank loans)

- HDB (bank loans, subject to both MSR and TDSR)

- Commercial properties

- Investment properties

- Refinancing and equity term loans (can be subject to prevailing concession/exemption rules and lender requirements)

For HDB concessionary loans, borrowers are generally assessed under the Mortgage Servicing Ratio (MSR) where applicable, together with HDB’s own eligibility criteria.

What Counts as Debt?

Many borrowers underestimate how much existing debt can affect their loan eligibility.

Banks typically consider obligations such as:

- Existing housing loan instalments

- Car loans instalment

- Renovation loans instalment

- Personal loans instalment

- Education loans instalment

- Credit card usage (typically based on minimum payment due)

- Student loans instalment

- Company facilities where you are standing as a personal guarantor (up to 20% of the monthly instalment or 100% if it is for an investment holding company)

- Other financial commitments such as interest servicing line/loan or any other facilities.

Even if you consistently make payments on time, these obligations reduce the amount available for servicing a new home loan.

What Counts as Income?

Not all income is treated equally.

Banks generally consider:

Employment Income (fixed, incept 100%)

- Basic salary

- Fixed monthly allowances

- Guaranteed allowances

Variable Income (up to 70%)

Subject to the bank’s assessment and supporting documents:

- Bonuses

- Commissions

- Overtime

- Incentive payments

Banks are required to apply a 30% haircut on these earnings over a period to assess sustainability.

Self-Employed Income

Self-employed borrowers are usually required to provide:

- Notices of Assessment (NOA)

- Bank statements

- CPF contribution history (if relevant)

Income is often assessed based on historical earnings rather than projected future income and might often come with a haircut.

Rental Income

Rental income may be recognised, but banks typically apply a haircut of 30% to account for any risks. Banks will ask for tenancy agreement (must have more than 6 months before expiry & certificate of stamp duty). Some banks might not incept rental income if rental income derive from subject property on proposed home loan request.

Dividend Income

Dividend income (haircut of 30% or more applicable) may also be considered if it is regular, well-supported by documentation, and meets the bank’s assessment criteria. Typically require at least 2 years of records, supported by dividend income proof, board resolution, dividend crediting proof etc.

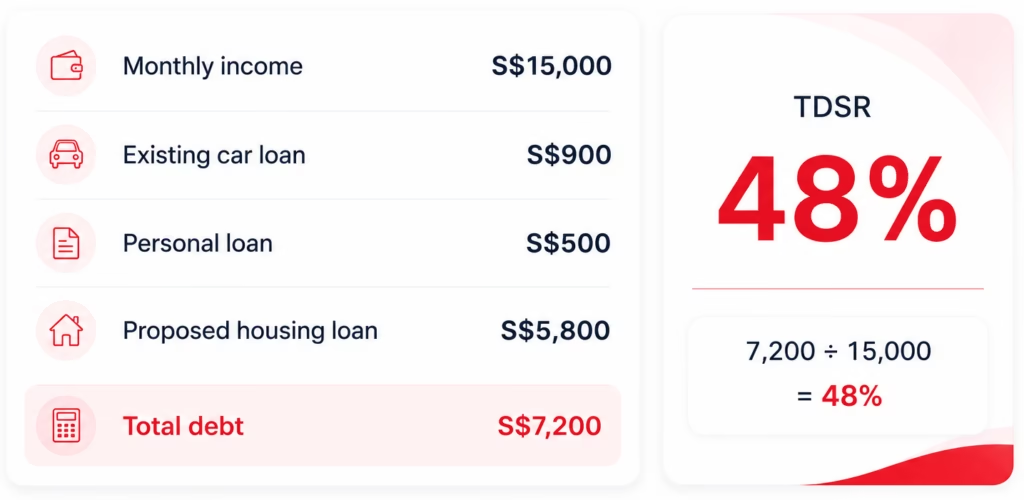

How Is Total Debt Servicing Ratio (TDSR) Calculated?

The formula is straightforward:

Example

This is below the 55% threshold, so the borrower would generally satisfy the TDSR requirement, subject to the lender’s overall assessment.

Common Reasons Why Buyers Receive a Lower Loan Than Expected

Many borrowers assume the bank will simply lend the maximum based on income.

In reality, there are several factors that can reduce the approved loan amount:

- Existing debt obligations

- Loan tenure restrictions

- Age of the borrowers

- Variable income adjustments

- Interest rate stress testing (usually apply a higher rate as compared to actual home loan interest rate)

- Remaining leasehold of subject property for the proposed home loan

- Credit assessment

- Property valuation

Does CPF Affect TDSR?

No.

Your CPF Ordinary Account balance is not treated as income for TDSR purposes.

However, CPF savings can still be used, subject to applicable CPF rules to pay eligible portions of the downpayment and monthly instalments after the loan is approved.

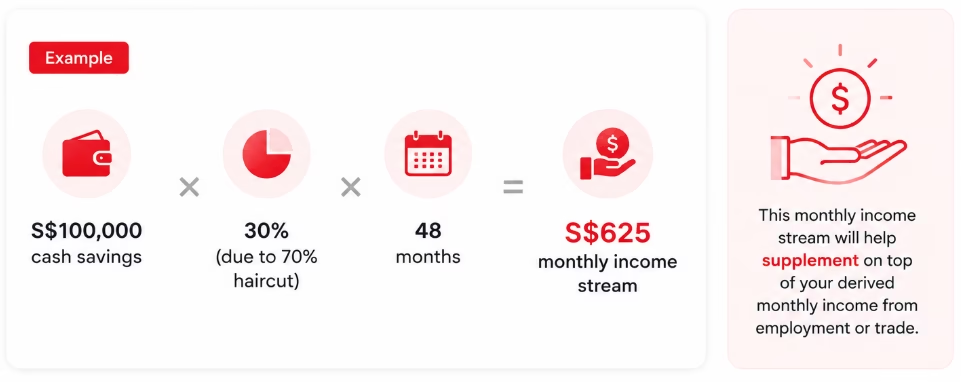

Does Cash Savings Increase My Loan Amount?

Not directly.

Having significant cash savings demonstrates financial strength, but it does not increase your TDSR.

Instead, cash savings may:

- Improve your ability to meet downpayment requirements

- Provide a financial buffer

- Support the lender’s overall credit assessment

However, cash savings or any other eligible financial assets can help to increase the loan amount, if the proposed cash savings are presented at the point of application and are expected to still be residing in your bank account after the purchase completion.

Example

The cash savings balance needs to be presented to the bank at the point of loan application and before the disbursement of the proposed housing loan.

What Happens If Interest Rates Rise?

Banks do not assess affordability solely using today’s promotional mortgage rate.

For regulatory purposes, lenders apply an interest rate floor, currently 4% for residential property financing and 5% for non-residential property financing.

This is known as the prevailing MAS medium-term interest rate floor, which is applicable for calculating loan affordability to ensure borrowers can cope if interest rates increase. The exact methodology is subject to prevailing regulatory requirements and the lender’s credit policies.

This is why the approved loan amount may be lower than expected, even when market mortgage rates are relatively low.

How Can You Improve Your Borrowing Capacity?

Borrowers may be able to improve their financing position by:

- Reducing Existing Debt

Paying off or reducing outstanding loan instalments can improve your debt servicing capacity. - Increasing Verifiable and Assessable Income

Where possible, ensure all eligible income is properly documented. - Applying Jointly

A joint application may increase combined assessable income, subject to the lender’s policies. - Choosing an Appropriate Loan Tenure

A longer tenure (within regulatory limits) may reduce monthly instalments, though it increases total interest over the life of the loan. - Planning Early

Speaking to a mortgage adviser before committing to a property can help identify financing options and avoid unexpected issues.

Frequently Asked Questions

Can freelance income be counted?

Yes, provided it can be adequately substantiated and meets the bank’s assessment criteria.

Does rental income count?

Often yes, but banks typically apply a haircut.

Does commission income count?

Yes, subject to documentation and the bank’s assessment of its consistency and sustainability.

Can I borrow until age 75?

Loan tenure and borrower age are subject to prevailing regulatory limits and the lender’s credit policies. Your age can affect both the maximum tenure and the amount you are eligible to borrow.

You can typically borrow beyond 65 years old, but will be subject to a loan-to-value cut and an increment of mandatory minimum cash component for the purchase of the property.

If I exceed the 55% TDSR, will my loan definitely be rejected?

Not necessarily. It could be a case of lowered loan eligibility rather than an outright loan rejection.

While the TDSR framework is an important regulatory requirement, lenders also consider other factors such as applicable regulations and their own credit assessment.

A mortgage specialist can help you understand your options based on your situation and financial profile.

Real-Life Example

Mr. & Mrs. Tan are upgrading from a 5-room HDB flat to a new condominium.

Combined monthly income: $18,000

Existing car loan: $1,100/month

No other outstanding loans.

Initially, they assumed they could comfortably finance their desired property.

After reviewing their TDSR, IQrate highlighted that the car loan reduced their borrowing capacity. By planning their financing early and understanding the impact of their existing commitments, they were able to set a realistic budget and proceed with greater confidence.

(Illustrative example only.)

Why TDSR Planning Matters

Many buyers only discover financing constraints after paying the Option to Purchase (OTP) fee or committing to a property.

Planning ahead allows you to:

- Understand your true affordability.

- Compare suitable financing options.

- Reduce the risk of delays or unsuccessful loan applications.

- Make informed decisions with confidence.

Common TDSR Mistakes

- Assuming CPF counts as income.

- Forgetting car loans reduces borrowing capacity.

- Using gross bonus instead of assessable income.

- Applying after changing jobs.

- Believing all banks assess income identically.

- Not declaring all financial commitments.

- Paying the OTP before confirming financing.

How IQrate can help you?

Before You Commit to Your Next Property…

Whether you’re buying your first home, upgrading from an HDB, investing in a condominium, or refinancing an existing loan, understanding your borrowing capacity is one of the most important steps.

At IQrate, we help homeowners compare financing options across multiple banks, assess affordability, and structure their home loans with confidence.

A 30-minute consultation today could save you thousands of dollars over the life of your mortgage. Reach out to an IQrate Mortgage Broker for a complimentary consultation and secure the lowest mortgage loan rates in Singapore.